Personal Finance

How Much Do You Actually Need to Retire? The 4% Rule, Explained Without the Maths Anxiety

This page may contain some affiliate links. This means that, at no additional cost to you, Alpha Investing Group will earn a commission if you click through and make a purchase. Learn more.

You can estimate how much you need to retire in about sixty seconds.

You don't need a spreadsheet, an advisor, or a finance degree. You need one rule of thumb, the 4 percent rule, and one piece of arithmetic you can do in your head. It won't be exact, but it gets you within shouting distance of the real answer, which is more than most people ever bother to work out.

So before the math anxiety kicks in, here's the whole thing in plain English.

The shortcut: how much do you need to retire? Multiply by 25

Start with the number you actually care about: how much you want to spend each year once you stop working.

The 4 percent rule says you can safely pull 4 percent of your savings in your first year of retirement. Flip that around and it becomes a shortcut. If 4 percent of your pot needs to cover a year of spending, then your pot needs to be 25 times that spending. That's the whole calculation, and it's why some people call it the "rule of 25."

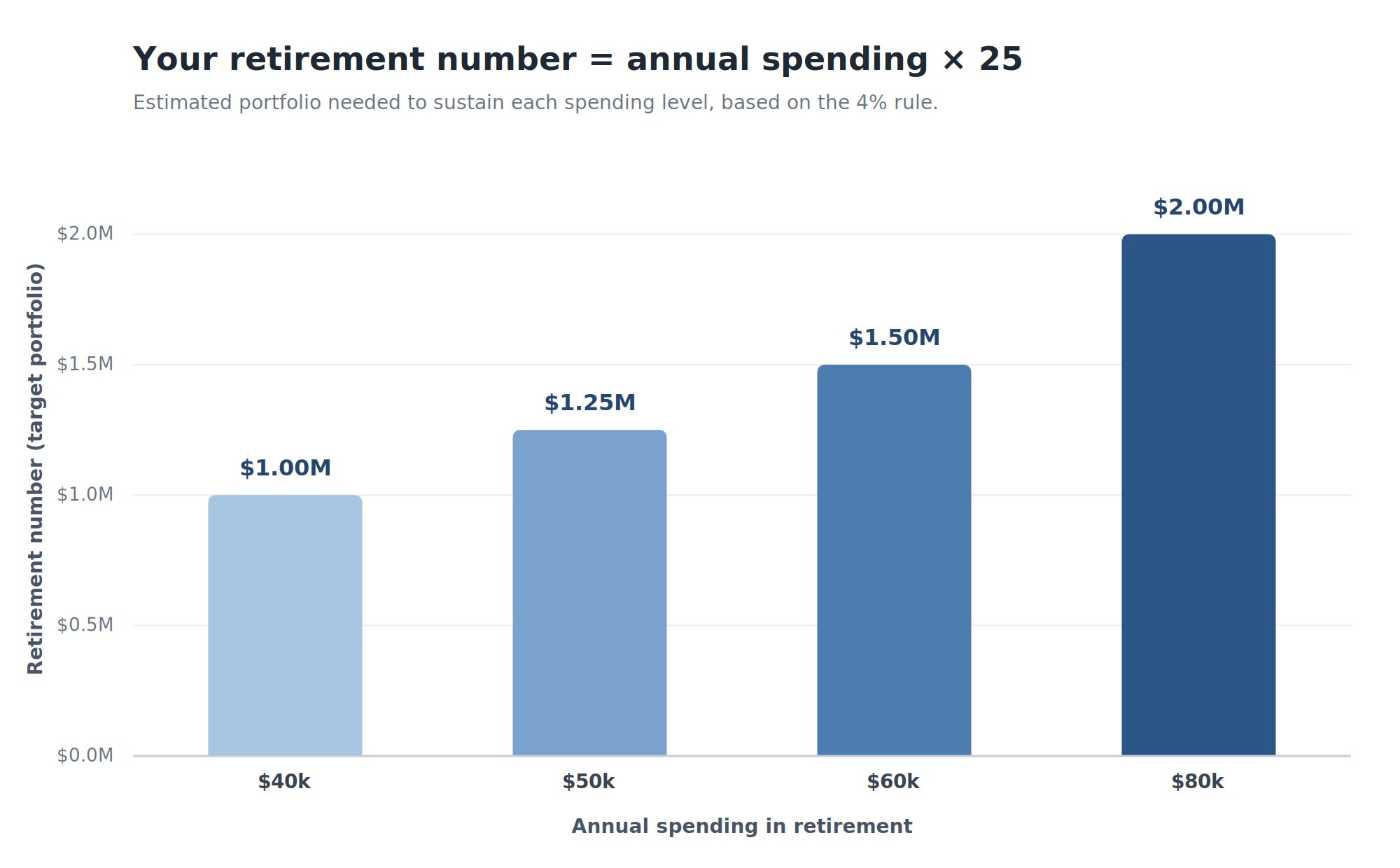

Here's how it lands at a few common spending levels:

- $40,000 a year to live on means a target of about $1.0 million.

- $50,000 a year means roughly $1.25 million.

- $60,000 a year means about $1.5 million.

- $80,000 a year means around $2.0 million.

The target retirement portfolio by annual spending level.

Notice what the number is not. It's not your salary times 25. It's the spending you'll fund from your portfolio, after any Social Security or pension does its share. That distinction takes a scary-looking figure and often shrinks it.

Where the 4 percent rule comes from

The rule isn't a guess. It's the result of someone running the historical numbers and writing them down.

In 1994, the financial planner William Bengen published a study in the Journal of Financial Planning that tested how much a retiree could withdraw without running out of money. He used a portfolio split evenly between stocks and bonds, and he ran it against the worst market stretches in modern US history, including someone who retired in 1968 right before a brutal decade. A 4 percent starting withdrawal, raised for inflation each year, survived a 30-year retirement in every case he tested. The Trinity Study, a few years later, reached much the same conclusion using similar data, and the rule of thumb stuck.

Two things matter in that origin story. The 4 percent figure assumes a balanced stock and bond allocation, not all cash and not all stocks. And it was built as a worst-case floor, not an average. Bengen himself has since said the typical safe rate has historically been closer to 7 percent, and he later nudged his own starting recommendation up toward 4.7 percent. The 4 percent number is deliberately cautious.

A worked example: $50,000 a year

Real numbers make this click faster than percentages do.

Say you want $50,000 a year from your investments. Multiply by 25 and your retirement number, the nest egg you're aiming at, is $1.25 million. In year one you withdraw $50,000, which is 4 percent of that pot.

The following year you don't recalculate 4 percent of the new balance. Instead you give yourself an inflation adjustment. If prices rose 3 percent, you take out $51,500, then bump it again the year after. The dollar amount drifts up with the cost of living, and the rule's job is to make sure the money keeps up for about three decades.

That inflation adjustment is the part people miss. The 4 percent is only the starting withdrawal rate. After that, your retirement spending tracks inflation, not the stock market, which is exactly why the rule needs a cushion built in. A portfolio built around a low-cost index fund is the usual engine behind these numbers, because low fees leave more of the return in your pocket to do the compounding.

Why the safe withdrawal rate keeps drifting below 4 percent

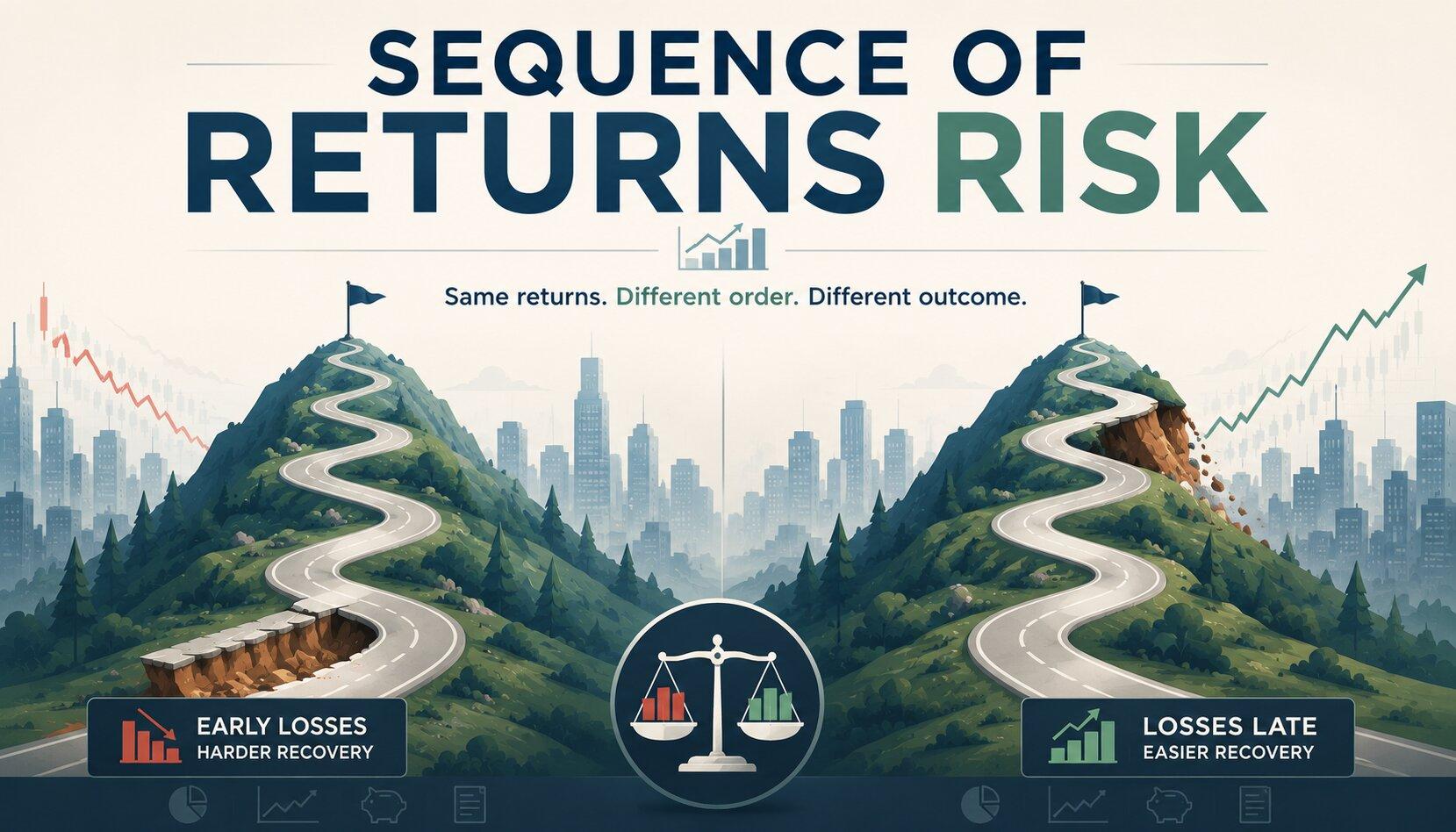

Here's the part the cheerful explainers skip. The "safe" number is a moving target, and lately it has been moving down.

The reason is something called sequence of returns risk, and it's the single most important idea here. Two retirees can earn the exact same average return over 20 years and end up in completely different places, purely because of when the bad years showed up. Schwab's illustration of sequence-of-returns risk shows it cleanly: an investor who hits a sharp market drop in the first two years of retirement can run out of money roughly a decade sooner than one who hits the same drop later. When you're selling investments to fund spending while prices are falling, you sell more shares to raise the same cash, and those shares never come back to ride the recovery.

That risk is why firms now publish starting rates below a flat 4 percent. Schwab's analysis of retirement spending puts the sustainable first-year withdrawal for a 30-year, moderate portfolio in a range around 3.7 to 4.8 percent in its 2026 estimates, partly because projected market returns for the next decade look lower than the long-run history Bengen used. None of this means the rule is broken. It means the honest version of the rule comes with a range, and the lower end of that range is the safer place to start.

What the rule quietly gets wrong

The 4 percent rule is a brilliant first cut. It's a terrible last word. Treat it as the napkin sketch, not the blueprint.

A few things it leaves out, and you should know about all of them:

- Taxes come out of the withdrawal, not on top of it. If you take $50,000 and owe $7,000 in taxes, you have $43,000 to actually spend. The rule guides the gross figure, so build your tax bill into the spending number you start with.

- It assumes rigid, robotic spending. Real retirees spend more some years and less in others, and most ease off as they age. A flexible withdrawal strategy that trims spending after a bad market year is safer than blindly raising it for inflation no matter what.

- It ignores Social Security and pensions. Both reduce how much your portfolio has to carry, which shrinks your target number. If Social Security covers $20,000 of a $50,000 lifestyle, your portfolio only needs to fund $30,000, so you multiply $30,000 by 25, not $50,000.

- It assumes a balanced, diversified portfolio. The 4 percent figure was never meant for an all-cash account or a single hot stock. It leans on a steady, passive approach and on rebalancing back to your target mix once a year so the risk stays where you set it.

None of these are reasons to ignore the rule. They're reasons to treat the number it gives you as the opening bid in a negotiation with reality.

In summary

The 4 percent rule is the fastest honest way to answer "how much do I need to retire," as long as you remember what it is and isn't.

- The shortcut: multiply the annual income you want from your savings by 25. That's your target number.

- The origin: Bengen's 1994 research found 4 percent, adjusted for inflation, survived a 30-year retirement on a balanced portfolio even through the worst historical stretches.

- The catch: sequence-of-returns risk and today's high valuations have pushed the safe starting rate toward the 3.7 to 4 percent end, so lean conservative.

- The fine print: it ignores taxes, healthcare, Social Security, and the fact that you're a human, not a formula.

Use it to get a number this week. Then refine it every year as your real life comes into focus.

FAQ

Does the 4 percent rule still work in 2026?

Yes, with a caveat. The rule itself still holds up against historical data, but most current research suggests starting nearer 3.7 to 4 percent rather than assuming a clean 4 percent is the ceiling. Today's stock valuations are high and projected returns over the next decade look lower than the long-run averages the rule was built on, which argues for the cautious end of the range and a willingness to adjust spending if markets disappoint early.

How much do I need to retire on $50,000 a year?

Roughly $1.25 million, using the multiply-by-25 shortcut. But that's the amount you need your portfolio to generate. If Social Security or a pension covers part of that $50,000, subtract it first. A retiree expecting $20,000 from Social Security only needs their savings to produce $30,000, which means a target closer to $750,000.

Is the 4 percent rule before or after tax?

Before tax. The withdrawal is a gross figure, and any income tax you owe comes out of it. If you want $50,000 to actually spend, you need to withdraw enough to cover both your spending and your tax bill, so build taxes into the number from the start rather than treating them as a surprise.

Does the 4 percent rule include Social Security?

No. The rule only describes what you draw from your investment portfolio. Social Security, a pension, or any other income stream sits on top and reduces how much your portfolio has to provide. That's good news, because it usually makes your real retirement number smaller than the headline figure the rule spits out.