Personal Finance

The Quiet Retirement Risk Most Investors Ignore (Until It's Too Late)

This page may contain some affiliate links. This means that, at no additional cost to you, Alpha Investing Group will earn a commission if you click through and make a purchase. Learn more.

Two people retire on the same day, each with the same $1 million.

They buy the same funds and take out the same amount every year. Over the next two decades the market even hands them the identical set of returns, just shuffled into a different order. Same average, same withdrawals, same everything.

One of them stays comfortable for life. The other runs out of money with years to spare, and the reason is sequence of returns risk.

Almost nobody plans for it.

It's the risk that the order of your returns, not just the average, decides whether your money lasts. It doesn't care how clever your fund picks were. It cares about when your bad years show up. So here's what it actually is, who should worry about it, and the boring fixes that beat panic every time.

What sequence of returns risk actually is

Start with a fact that feels wrong: the average return can lie to you.

If a portfolio earns 6% a year on average, you'd expect two people earning that same 6% to end up in the same place. They don't, once they start pulling money out. A steep drawdown in the first year or two forces you to sell more shares to raise the same cash, and those shares never get to recover. You've locked the loss in.

That's the whole idea. A bear market hurts at any age. But a bear market in the first years of retirement, while you're actively spending, does permanent damage that the same one ten years later doesn't.

Why the order matters when you're spending, not saving

Here's the part that trips people up. Sequence risk barely exists while you're still saving.

When you're contributing every month and touching nothing, a crash is a gift. Your paycheck keeps buying shares at lower prices, and by the time you retire those cheap shares have grown. This is the quiet logic behind passive index investing: keep buying, ignore the noise, let time do the work. A 20-year-old should almost hope for a few brutal years early on.

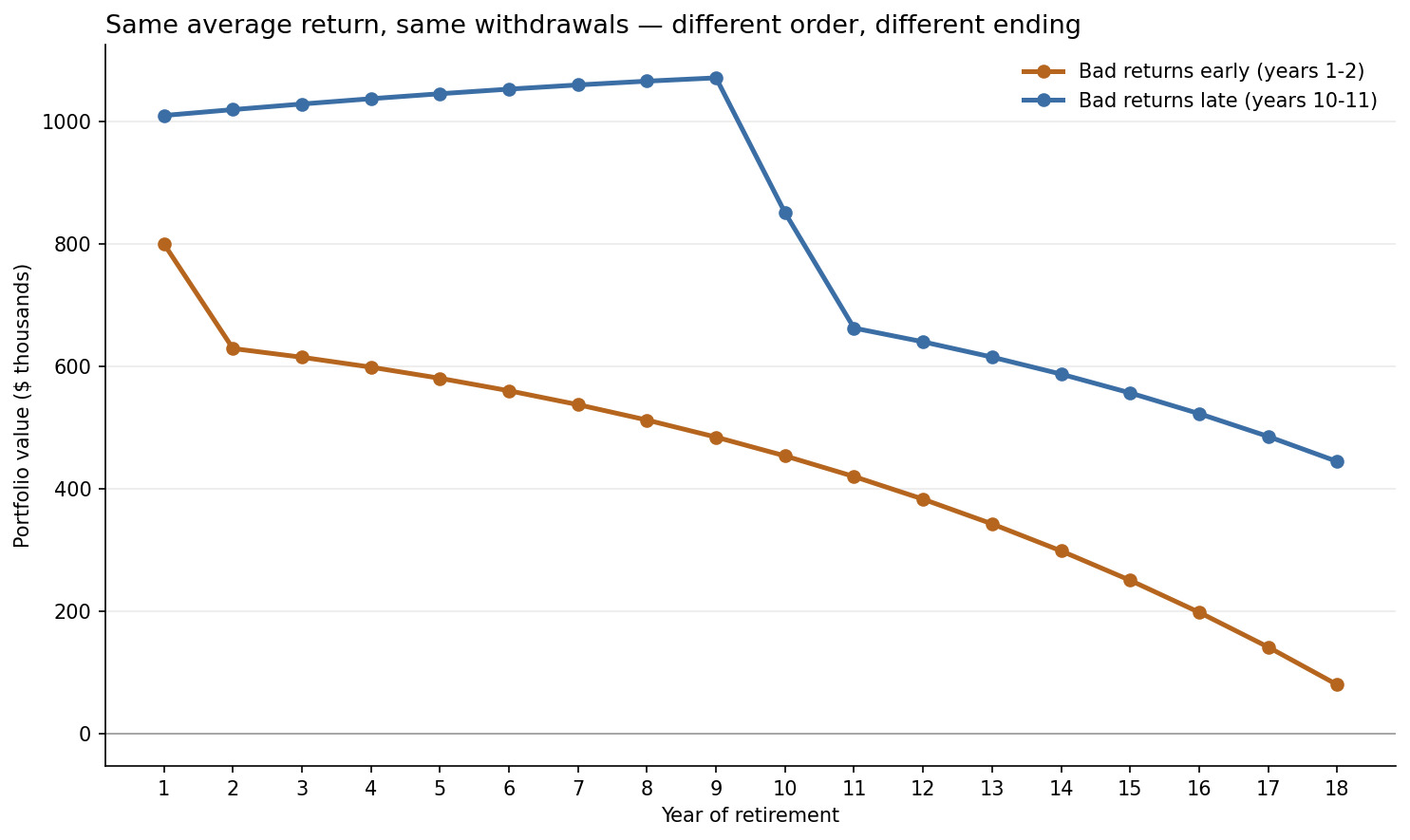

Flip to retirement and the math inverts. Now you're selling, not buying. Two identical $1 million portfolios take the same $50,000 withdrawals, adjusted up for inflation, and earn the same returns. The only difference is timing.

Figure 1: Impact of Return Sequencing on Retirement Portfolio Value

The retirement portfolio that hit its rough patch early ends up with a fraction of what its twin kept. The pattern mirrors Schwab's illustration of sequence-of-returns risk, which runs two investors through the same setup and finds one going dry while the other still holds close to $400,000.

The retirement risk zone: when sequence risk actually bites

Not every year of retirement is equally dangerous. There's a window that matters far more than the rest.

Researchers Wade Pfau and Michael Kitces call it the retirement risk zone, the roughly ten years on either side of your retirement date. Their research on a rising equity glidepath explains why this decade carries so much weight. Three things line up at once: your portfolio is at its largest, you've just started withdrawing, and you have the least time left to recover from a bad run. A crash then reshapes everything that follows. A crash twenty years earlier or twenty years later barely registers.

That's a strangely comforting idea once it lands. You don't have to fear the market forever. You have to respect one specific decade.

Who should actually worry, and who shouldn't yet

This is where most articles fail you, because most are written to sell a product. So let me be blunt about it.

If you're 35 with $80,000 saved and thirty years of contributions ahead, sequence of returns risk is not your problem right now. A crash next year is a sale, not a threat. The worst thing you can do is let a risk that belongs to your late 50s scare you out of the market in your 30s, which is just trend-chasing wearing a serious face. Keep buying.

The people who should genuinely pay attention are the ones inside or approaching that risk zone. Roughly age 55 and up. Anyone who plans to retire in the next decade, or already has. If that's you, the good news is that the fixes are simple and you probably already own most of the pieces.

How to protect against sequence of returns risk

You don't beat sequence risk by predicting the market. You beat it by making sure you're never forced to sell at the bottom. Three moves do almost all the work.

First, build a cash buffer. Hold a year or two of spending in cash and another few years in short-term bonds, so a bad market never forces you to sell stocks to eat. Schwab suggests keeping about a year of expenses in cash and two to four years in high-quality short-term bonds. That reserve is what lets the rest of your money ride out a downturn instead of getting sold into it.

Second, use a bond glidepath. Carry more bonds going into retirement, then let your stock share drift back up once the risky decade is behind you. This "bond tent" is the practical version of the Pfau and Kitces finding: hold your most defensive mix exactly when you're most exposed, then get more aggressive again later. Ordinary portfolio rebalancing keeps the shape honest year to year.

Third, stay flexible on what you withdraw. The 4% rule gives you a starting safe withdrawal rate, and Morningstar's 2026 retirement income research currently pegs a cautious version closer to 3.9% over a 30-year horizon. But the real protection is simply spending a little less in the bad years. Skip the inflation raise after a down market and you take enormous pressure off the portfolio. Retirees who can flex their spending can safely start much higher than those who can't.

None of this is exotic. There's no market-timing call and no crystal ball. It's a reserve, a sensible mix, and the willingness to tighten your belt for a year or two.

The honest take

Here's what gets me about how this topic usually gets sold.

The typical article defines sequence risk, shows you one scary chart, and then funnels you toward an expensive annuity or an advisor's calendar. The fear is real, so the pitch works. But buying a costly product to insure against a risk you could handle with a cash buffer and some spending flexibility is its own mistake. You're paying a permanent fee to avoid a temporary problem.

Sequence risk is more behavioral than mathematical anyway. The retirees who get hurt aren't the ones who saw a bad market. They're the ones who panicked, sold at the bottom to fund an unchanged lifestyle, and never recovered. The whole game is avoiding a forced sale, then not talking yourself into a voluntary one. That's a discipline problem, not a product problem.

So respect the risk zone. Prepare for the decade that matters. Then stop treating a manageable, well-understood risk like a reason to hand your money to whoever markets the loudest.

Frequently asked questions

Does sequence of returns risk matter before I retire?

Not really. While you're still saving and adding money, the order of returns has little effect, because you're buying through the dips instead of selling into them. A down market in your accumulation years can even help, since your contributions buy more shares cheaply. Sequence risk switches on when you flip from adding money to withdrawing it.

Is sequence of returns risk the same as market timing?

No. Market timing is trying to guess when to jump in and out of stocks, which rarely works. Managing sequence risk is the opposite: you assume you can't predict the market, so you build a structure (a cash buffer, a bond glidepath, flexible withdrawals) that keeps a bad run from forcing your hand.

Do I need an annuity to protect against it?

Not necessarily. An annuity can turn some savings into guaranteed income, which removes sequence risk from that slice, and for some people the peace of mind is worth it. But a cash reserve and spending flexibility address the same risk at far lower cost. Don't buy an expensive product out of fear before you've looked at the cheaper tools.

Doesn't the 4% rule already handle this?

Largely, yes. The 4% rule that William Bengen published in 1994 was built around a worst-case retiree who faced a rough market and high inflation right at the start. In other words, it was stress-tested against a bad sequence from day one. A sensible safe withdrawal rate plus a little flexibility already covers most of the danger. Sequence risk is the reason the rule is that cautious in the first place.

This article is educational and not personalized investment advice. All investing carries risk, including possible loss of principal, and past performance doesn't predict future results.