Personal Finance

What to Do With Your Tax Refund Before You Spend It (A 5-Step Decision Tree for Your 20s and 30s)

This page may contain some affiliate links. This means that, at no additional cost to you, Alpha Investing Group will earn a commission if you click through and make a purchase. Learn more.

A tax refund feels like a gift. It isn't.

If you've been searching what to do with tax refund money this spring, here's the part most articles skip: that check is your own salary, handed back to you after the government held it for a year without paying you a cent of interest. Knowing that changes everything about how you should use it. It's not found money to blow on a trip, and it's not a reward for filing on time.

So before lifestyle inflation quietly claims it, run your refund through a simple decision tree.

- Clear any high-interest debt first

- Top up your emergency fund to a real cushion

- Feed a prior-year IRA while the deadline is open

- Invest whatever's left for the long haul

- Keep a small slice for something that actually makes you happy

Do these in order and a $1,500 check does more for you than a $5,000 one ever does for someone who spends it on autopilot.

First, understand why your refund isn't free money

Here's the mental trap. Your brain files a refund in a different account than your paycheck, even though every dollar is identical.

Economists call this mental accounting, and the St. Louis Fed's explainer on how mental accounting shapes our choices uses the tax refund as its central example. We treat refunds as windfalls, label them "found money," and spend them far more freely than we'd ever spend the same amount from our salary. That's the windfall effect at work. The Fed's piece is blunt about the fix: from a rational standpoint, a refund is just money you've owned all along, and using it to pay down high-interest debt is almost always the smartest move.

The numbers make it worth caring about. IRS filing-season data shows the average federal refund topped $3,000 in 2026. For a 26-year-old, that's not pocket change. It's a month of rent, or a real safety net you didn't have last week.

A big refund isn't even good news. It means you handed the government an interest-free loan all year. FINRA's rundown of smart refund moves makes the same point and tells you to fix it. More on that at the end.

So treat the money like the income it is. Then put it to work in order.

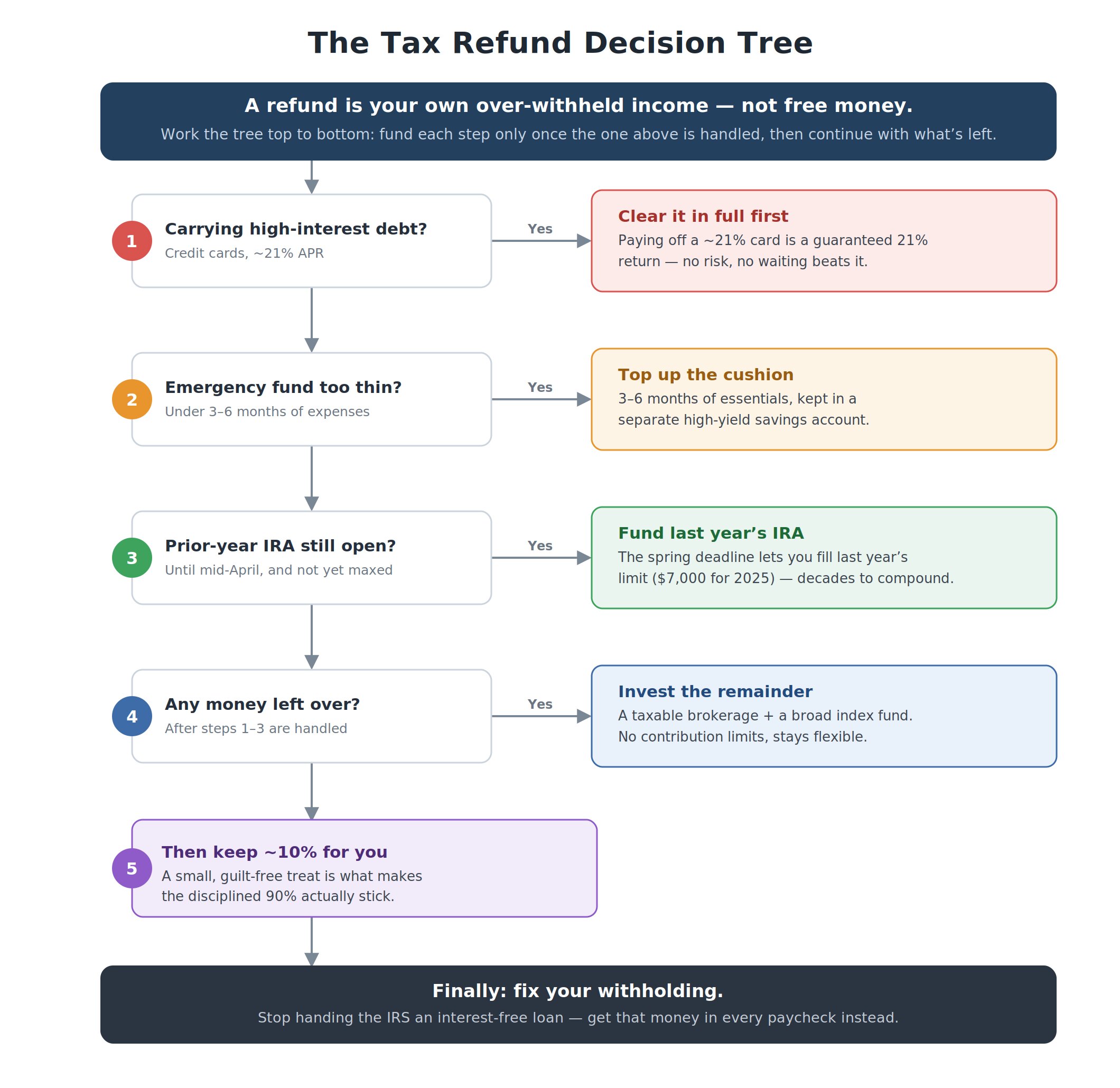

The tax refund decision tree, in five steps

The reason most refund advice fails isn't that the tips are wrong. It's that they're a menu, not an order.

You get handed twelve "smart things to do" and no way to choose between them. A decision tree fixes that. You start at the top, and you only move down a step once the one above it is handled. For most people in their 20s and 30s, the order below is the one that puts the most money back in your pocket. Each step beats the one after it on guaranteed value.

Work through it top to bottom.

Step 1: Wipe out high-interest debt

First, look at what you owe. If you're carrying a credit card balance, this is where your refund goes. All of it, if that's what it takes.

The reason is pure math. The Federal Reserve's data on credit card rates puts the average card APR at around 21%. Paying off a balance charging 21% is the same as earning a guaranteed 21% return on that money, with no risk and no waiting. There's no investment on earth that reliably beats that. A good rule of thumb: any high-interest debt above about 7% gets cleared before you invest a dollar, and credit cards blow right past that line.

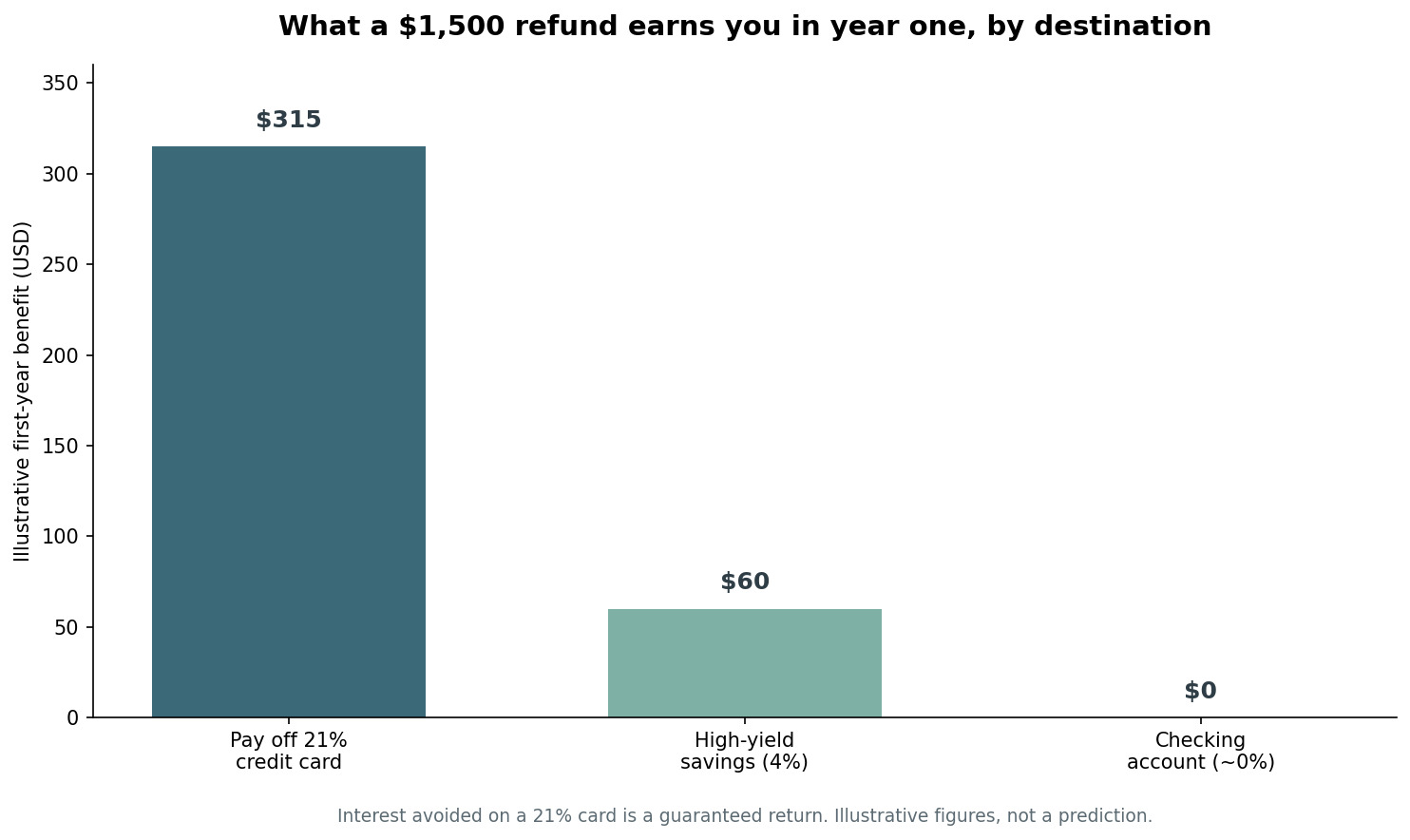

Figure 1: Bar chart of the illustrative first-year benefit of a $1,500 refund by destination: paying off a 21% credit card (about $315 in interest avoided) vs a high-yield savings account at 4% (about $60) vs a checking account (about $0).

Look at what that means in dollars. Put $1,500 against a 21% card and you avoid about $315 in interest over the next year alone. Park the same $1,500 in a high-yield savings account and you might earn $60. Leave it in checking and you earn basically nothing. Same money, wildly different outcomes, and the highest-return option is the boring one. If debt is the thing standing between you and breathing room, our guide to getting out of debt for good walks through how to attack it after the refund runs out.

Clear the high-interest stuff. Then keep going.

Step 2: Top up your emergency fund

Second, build your buffer. If you don't have one yet, your refund is the fastest way to start.

An emergency fund is the cash that stops a flat tire or a surprise medical bill from becoming credit card debt, which would just drag you back to Step 1. The standard target is three to six months of essential expenses, and FINRA points to that same range. You don't need to hit it all at once. Even one month of expenses in a separate high-yield savings account changes how a bad week feels.

A trick that works: have the money direct-deposited somewhere slightly annoying to reach, so it doesn't leak into everyday spending. If you're starting from zero, our emergency fund guide breaks down how much you actually need based on your situation.

Debt's gone, cushion's growing. Now the money can start working for the future.

Step 3: Feed a prior-year IRA while you still can

Third, and this one is time-sensitive, consider a prior-year IRA contribution.

Here's the quirk most people miss. You can contribute to an IRA for the previous tax year right up until the filing deadline in mid-April. So a refund that lands in spring can be funneled straight into last year's contribution limit before that window closes, on top of what you put in for the current year. The IRS's IRA contribution limits were $7,000 for the 2025 tax year, and the 2026 limit rose to $7,500. If you tell your provider the contribution is for the prior year, it counts against that year's cap.

Why bother in your 20s? Time. A contribution you make at 26 has four decades to compound before you retire, which is the biggest edge a young investor gets. You don't need to pick anything clever. A low-cost, broadly diversified fund inside the account is enough, and lining the refund up with your wider financial goals in your 20s keeps it from being a one-off.

Retirement's funded. If there's still money left, it goes to work too.

Step 4: Decide where to put what's left

Fourth, once debt, emergencies, and retirement are handled, the question becomes where to put tax refund money that's still sitting there.

A regular taxable brokerage account is the answer for most people. It doesn't have the tax perks of an IRA, but it also has no contribution limit and no withdrawal rules, so the money stays flexible for medium-term goals: a house down payment, a career break, a wedding. Buy a broad index fund, set it, and leave it alone. This is also where a sensible personal budgeting system helps, because it tells you how much of the refund you genuinely don't need for the next few years.

Most 20-something refunds never make it to Step 4, and that's fine. Steps 1 to 3 are where the real wins are.

Step 5: Spend some of it on purpose

Fifth, keep a slice for yourself. Roughly 10%.

This isn't a reward you have to earn. It's strategy. A plan you hate is a plan you'll abandon, and earmarking a small, guilt-free chunk for something you actually want makes the disciplined 90% stick. The research on spending tends to favor experiences over stuff, so a concert or a weekend away usually delivers more lasting happiness than another gadget. The point is that you chose it on purpose, instead of letting the whole refund dribble away on nothing you'll remember.

Spend the 10%. Mean it. Then protect the rest.

A worked example: one $1,500 refund through the tree

Numbers make this concrete, so here's a typical case.

Say you're 26, you just got a $1,500 refund, and you're carrying an $800 balance on a credit card at 21%. Run the tree. Step 1 takes $800 to wipe out the card, which saves you roughly $170 in interest over the next year and frees up the minimum payment you were making. That leaves $700.

You've got about half a month of expenses saved, so Step 2 takes the next $500 into your emergency fund, nudging you toward a real cushion. That leaves $200. You direct $150 of it into a prior-year IRA at Step 3, getting four decades of compounding on money that would otherwise be gone by summer. The last $50 is yours, guilt-free, at Step 5.

One $1,500 check just erased a debt, built a buffer, started a retirement account, and still paid for a nice dinner. That's what order does.

A quick note on what to do with a tax refund in your 30s

The tree doesn't change much in your 30s, but the weights do.

By then you may have a bigger income, a mortgage, or kids in the picture, which shifts the emphasis. High-interest debt still comes first, always. But your emergency fund target probably climbs toward the six-month end of the range, and Step 4 may include a 529 college account or a larger down-payment fund. The order holds. The dollar amounts at each step just get bigger.

The last move: stop giving the IRS an interest-free loan

Now circle back to where the money came from.

A refund means you overpaid your taxes all year, so the government held your cash for twelve months and gave it back without interest. The cleaner setup is to get that money in each paycheck instead, where you can use it to pay down debt or invest as you go. A quick withholding adjustment is how you do it. The IRS Tax Withholding Estimator walks you through your numbers and spits out a pre-filled W-4 you can hand to your employer.

There's one honest exception. If a forced refund is the only way you reliably save, the lost interest might be a fair price for the discipline. Just make that a choice, not an accident.

In summary

Here's the whole decision tree as a checklist you can run every spring:

- Reframe it. A refund is your own over-withheld money, not free money. Treat it like income.

- Step 1, high-interest debt. Clear credit cards first. Paying off 21% is a guaranteed 21% return.

- Step 2, emergency fund. Build toward three to six months of expenses in a separate account.

- Step 3, prior-year IRA. Use the spring deadline to fund last year's limit and buy decades of compounding.

- Step 4, invest the rest. A taxable brokerage account keeps medium-term money growing and flexible.

- Step 5, spend 10% on purpose. A small, deliberate treat is what makes the other 90% stick.

- Then fix your withholding so next year's raise shows up in your paychecks instead of a refund.

Figure 2: The Tax Refund Decision Tree: five ordered steps for using your refund

The smartest thing you can do with a refund isn't a single clever move. It's running the money through the same boring order, every single year, before your brain files it as found money and spends it for you.

Frequently asked questions

Should I use my tax refund to pay off debt or invest it?

Pay off high-interest debt first, almost every time. With the average credit card charging around 21%, clearing that balance is a guaranteed 21% return that no investment can reliably match. Once your high-interest debt is gone and you have a small emergency fund, then investing the rest through an IRA or brokerage account makes sense.

Can I still contribute to last year's IRA with my refund?

Often, yes. The IRS lets you make prior-year IRA contributions up until the tax filing deadline in mid-April. If your refund arrives before then, you can direct it into the previous year's contribution limit, as long as you tell your provider it's a prior-year contribution. Check the current IRS limits before you contribute.

Is a tax refund free money, and should I be happy about a big one?

It's not free money. A refund is your own income that you overpaid during the year, returned to you without interest. A large refund actually means you gave the government an interest-free loan. It's not a windfall to celebrate so much as a sign your withholding is set too high.

How do I stop getting such a big refund every year?

Adjust your tax withholding. The IRS Tax Withholding Estimator helps you calculate the right amount and generates a pre-filled W-4 to give your employer. The result is a bigger paycheck during the year, money you can save or invest immediately instead of waiting for it back at tax time.

Is it okay to spend some of my refund on something fun?

Yes, and it's smart to plan for it. Setting aside roughly 10% for something you genuinely enjoy makes the disciplined use of the other 90% far more likely to stick. The trick is choosing it on purpose, rather than letting the entire refund slip away on things you won't remember.

This article is educational and not personalized financial advice. Investing involves risk, including possible loss of principal, and the figures here are illustrative, not predictions or guarantees.