Personal Finance

What's a Good Credit Score, Really? The Three Numbers That Actually Change Your Life

This page may contain some affiliate links. This means that, at no additional cost to you, Alpha Investing Group will earn a commission if you click through and make a purchase. Learn more.

The good credit score range everyone talks about is wider than the part that actually matters.

It's a set of thresholds, and the band lenders actually reward is narrower than the credit industry lets on. Most explainers hand you a chart of five tiers from 300 to 850 and tell you higher is better, which is true and nearly useless. What you want to know is which numbers change the price of borrowing, and which ones are vanity.

There are three that matter.

What a good credit score range actually means

Almost every score you'll see runs from 300 to 850. The FICO scoring bands split that scale into five tiers, and FICO scores sit behind about 90% of top lending decisions, so these are the labels that count:

- Poor: below 580. Seen as high risk. Approvals are limited and pricing is steep.

- Fair: 580 to 669. Below the US average. Many lenders will still say yes, but not at good rates.

- Good: 670 to 739. Near or just above the typical borrower. This is where mainstream credit opens up.

- Very Good: 740 to 799. Above average. You start getting the better pricing, not just approval.

- Exceptional: 800 to 850. Top tier, lowest risk in the eyes of a lender.

Here's the part the tier chart hides. The jumps between these bands are not evenly valuable. Crossing from Fair into Good changes your life. Crossing from 800 to 840 changes almost nothing. So the useful question isn't "what tier am I in," it's "which lines are worth crossing."

The three numbers that change your life

Strip away the five-color chart and three thresholds are doing nearly all the work.

- Around 670: the door opens. This is the line between "subprime pricing and frequent declines" and "a normal borrower." Cross 670 and you become a prime borrower in the eyes of most lenders. Mainstream cards, normal auto loans, and standard apartment approvals start saying yes.

- Around 740: the price drops. This is where you stop merely qualifying and start getting good pricing. On big loans, especially a mortgage, 740 is the point where lenders quietly hand you a better rate. It's the single most valuable line on the whole scale.

- Around 760: the best pricing locks in. Most lenders reserve their very best terms for somewhere between 760 and 780, and a super prime borrower above that ceiling is treated as essentially zero risk. Past this point, the rate sheet stops improving.

Notice what's missing from that list. 850. Nobody at the lending desk cares whether you're an 805 or an 850. The marginal value above the high 700s rounds to zero.

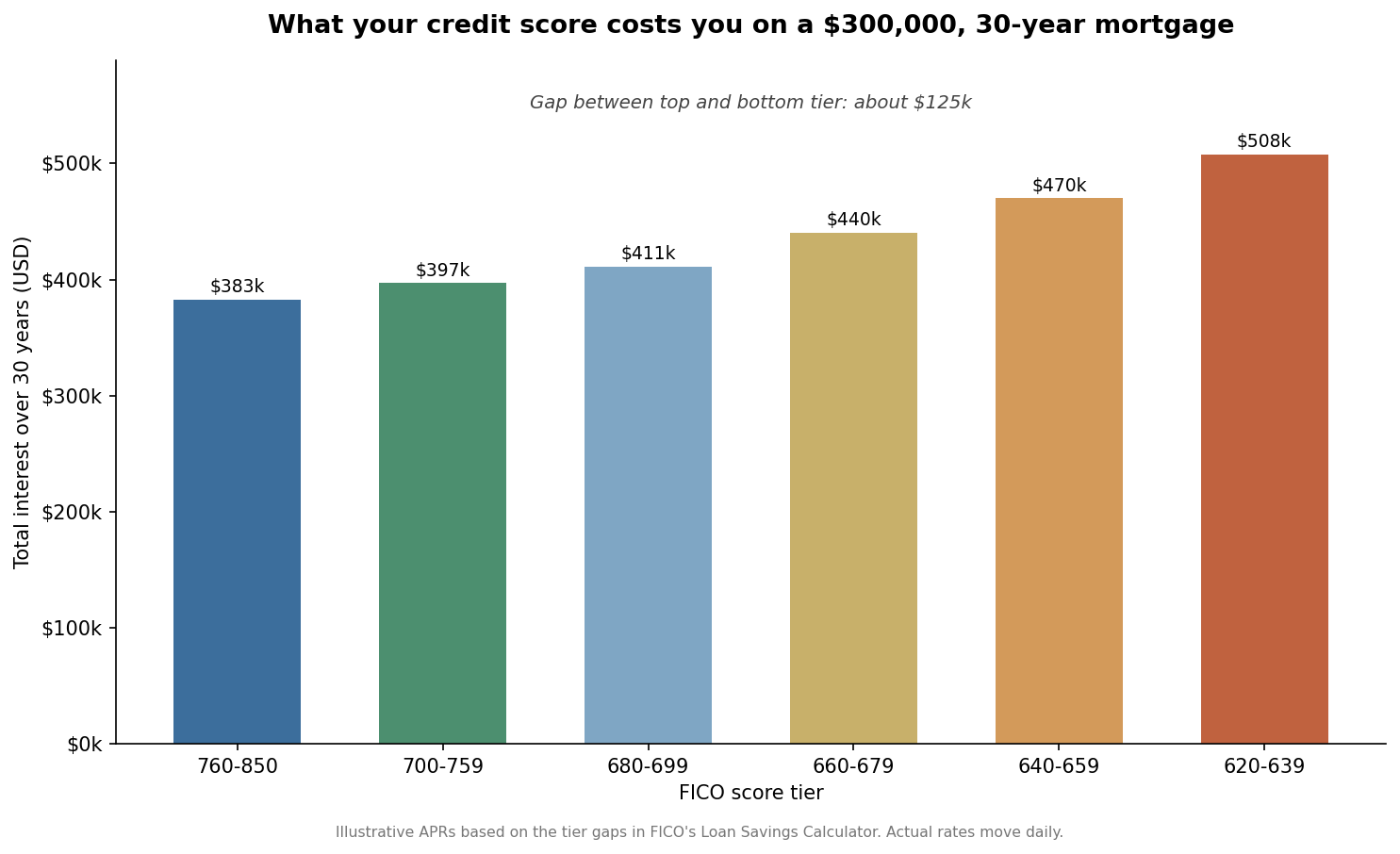

What your credit score is worth on a mortgage

Here's where the abstract tiers turn into real money. It's also the part almost no explainer bothers to work out.

Take a $300,000 home loan over 30 years. Your score doesn't change the house, the down payment, or the loan amount. It changes one thing: the interest rate. And on a balance that size, held for that long, small rate gaps compound into large numbers. Experian's data on mortgage rates by credit score shows the same pattern every year, with each tier paying a little more than the one above it.

Run illustrative rates through the math and the gaps are stark. A borrower above 760 might pay around $383,000 in lifetime interest. A borrower at 660 to 679 pays closer to $440,000. That's about $57,000, for the same loan, on the same house, decided almost entirely by a three-digit number. The borrower scraping in at 620 to 639 pays north of $500,000.

You don't need a perfect score to capture most of that benefit. You need to clear 740, and ideally 760. The climb from 760 to 850 is barely worth measuring. The climb from 660 to 740 is worth a car.

Why chasing 850 is mostly wasted effort

I'll be blunt, because the credit-influencer world won't. Treating your score like a video game high score is a misallocation of attention.

Once you're comfortably into the Very Good band, the lender world has already given you everything it's going to give. The best mortgage pricing tends to arrive a notch below the "Exceptional" label, often around 760 to 780, not at some heroic 820. Squeezing out the last 60 points usually means babysitting your utilization to the decimal and obsessing over report-pull timing, all for a rate that doesn't move. That effort is better spent on the things a high score is supposed to free you up for, like clearing high-interest debt or actually investing.

A high number also isn't a personality trait. It's a measure of how predictably you repay borrowed money, nothing more. It's worth understanding what a strong score does and doesn't say about your financial health before you wrap your identity around it.

What actually moves your score

If you do want to climb, the levers aren't a mystery, and they aren't equally weighted. According to myFICO's breakdown of what goes into a score, two factors dominate:

- Payment history (35%). Paying on time, every time, is the single biggest input. One missed payment can undo months of progress, so automate the minimums and never let a due date slip.

- Credit utilization (30%). This is how much of your available credit you're using. The CFPB's guidance on keeping a good score advises staying under 30% of your limit, and under 10% is better. It's also the fastest lever, because it updates in a billing cycle or two rather than over years.

- Length of history (15%), new credit (10%), and credit mix (10%). These move slowly. The mix of cards and loans you carry, the age of your accounts, and how often you apply round out the score, but they're not where quick gains live.

The practical takeaway: if you want movement in the next two months, pay every bill on time and pay your card balances down before the statement closes. Everything else is patience. For the day-to-day habits behind this, our guide to credit card strategies goes deeper.

Where the numbers get messy

Now the honest caveats, because the tidy chart skips them.

First, there isn't one score. FICO is the dominant model, but VantageScore uses the same 300 to 850 scale with different band cutoffs, and lenders pull different versions for different products. The score your free app shows you is rarely the exact one your mortgage lender sees.

Second, your number moves by bureau. Experian, Equifax, and TransUnion don't all hold identical data, so the same person can show three different scores on the same day. Experian's read on the average US score puts the typical FICO around 715, but yours can swing 20 to 40 points between bureaus for reasons you didn't cause.

Third, the thresholds I gave you are conventions, not laws. Lenders set their own cutoffs, and they drift with the economy. The 670, 740, and 760 lines are where the pricing tends to break, not promises any single bank has to honor.

None of that changes the core lesson. The bands are fuzzy, but the shape is reliable: a few thresholds carry almost all the value, and the top of the scale carries almost none.

In summary

A good credit score isn't a finish line at 850. It's three doors:

- ~670 turns you into a prime borrower and opens mainstream credit.

- ~740 is the highest-value line on the scale, where big-loan pricing actually improves.

- ~760 to 780 locks in the best terms most lenders offer. Above that, the rate sheet stops moving.

The whole game is clearing those lines and then getting on with your life. On a real mortgage, that's the difference between paying for one house and paying for one and a half. Chasing the last 60 points to a perfect score is the financial equivalent of polishing a trophy nobody will ever ask to see.

Frequently asked questions

Is a 700 credit score good?

Yes. At 700 you're inside FICO's "Good" band (670 to 739) and above the US average of roughly 715's lower neighbors, so you'll qualify for mainstream credit. You're not yet at the 740 line where the best big-loan pricing kicks in, so it's a solid base with one more worthwhile threshold ahead.

Does checking your credit score lower it?

No. Checking your own score is a "soft" inquiry and has no effect. Only "hard" inquiries from a lender reviewing a new application can ding it, and even then only slightly. Rate shopping is protected too: the CFPB notes that multiple inquiries for the same loan type within a 14 to 45 day window generally count as one.

How long does it take to build a good credit score?

From scratch, FICO generally needs at least one account that's been open about six months before it can score you. Reaching the "Good" band usually takes a year or more of on-time payments and low utilization. If you're repairing damage, the fastest gains come from paying down card balances, which can show up in a billing cycle or two.

What's the difference between a FICO score and a VantageScore?

Both run 300 to 850, but they're built by different companies with slightly different rules and band cutoffs. FICO is used in the large majority of lending decisions, especially mortgages, while VantageScore often powers the free scores in banking apps. Treat your free VantageScore as a directional gauge, not the exact number a mortgage lender will pull.