Investing

Should You Pay Off Your Mortgage Early or Invest the Difference? Here's the Maths

This page may contain some affiliate links. This means that, at no additional cost to you, Alpha Investing Group will earn a commission if you click through and make a purchase. Learn more.

A 6.5% mortgage changes the conversation. A few years ago, with rates near 3%, the maths said invest and barely look back. Today the gap between paying down your loan and chasing market returns is much smaller, which means the decision to pay off mortgage or invest matters again. The good news is that this is not a feeling. It is a calculation, with one behavioural tiebreaker on top.

The rest of this guide goes in order. First, the few things to do before you choose either option. Then the one comparison that settles it, your mortgage rate against your expected return. After that comes the tax angle most guides get wrong, the honest weight of being debt-free, a worked example you can copy, and the hybrid rule most people should default to.

Before you choose: do these three things first

The mortgage-versus-investing question only makes sense once your financial base is solid. Spend your extra money in the wrong order and the maths below stops mattering, because a single emergency can undo years of progress.

Do all three of these before you send a dollar to either the mortgage or the market:

- Capture every bit of your employer 401(k) match. A match is an instant 50% or 100% return on your money. Nothing in this article beats free money, so this comes first, always.

- Clear high-interest debt. Credit cards at 20%+ make a 6.5% mortgage look like a gift. Pay those off before you even open this debate.

- Build an emergency fund. Three to six months of expenses in cash means you never have to raid investments or miss a mortgage payment when the car breaks or the job ends.

Once those are handled, you have genuine extra cash flow to direct. Now the question is real.

The simple maths: your mortgage rate vs your expected return

Forget the emotion for a second. The decision is one comparison. On one side is the guaranteed return of paying down your loan. On the other is the expected return of investing the same money. Whichever number is bigger usually wins.

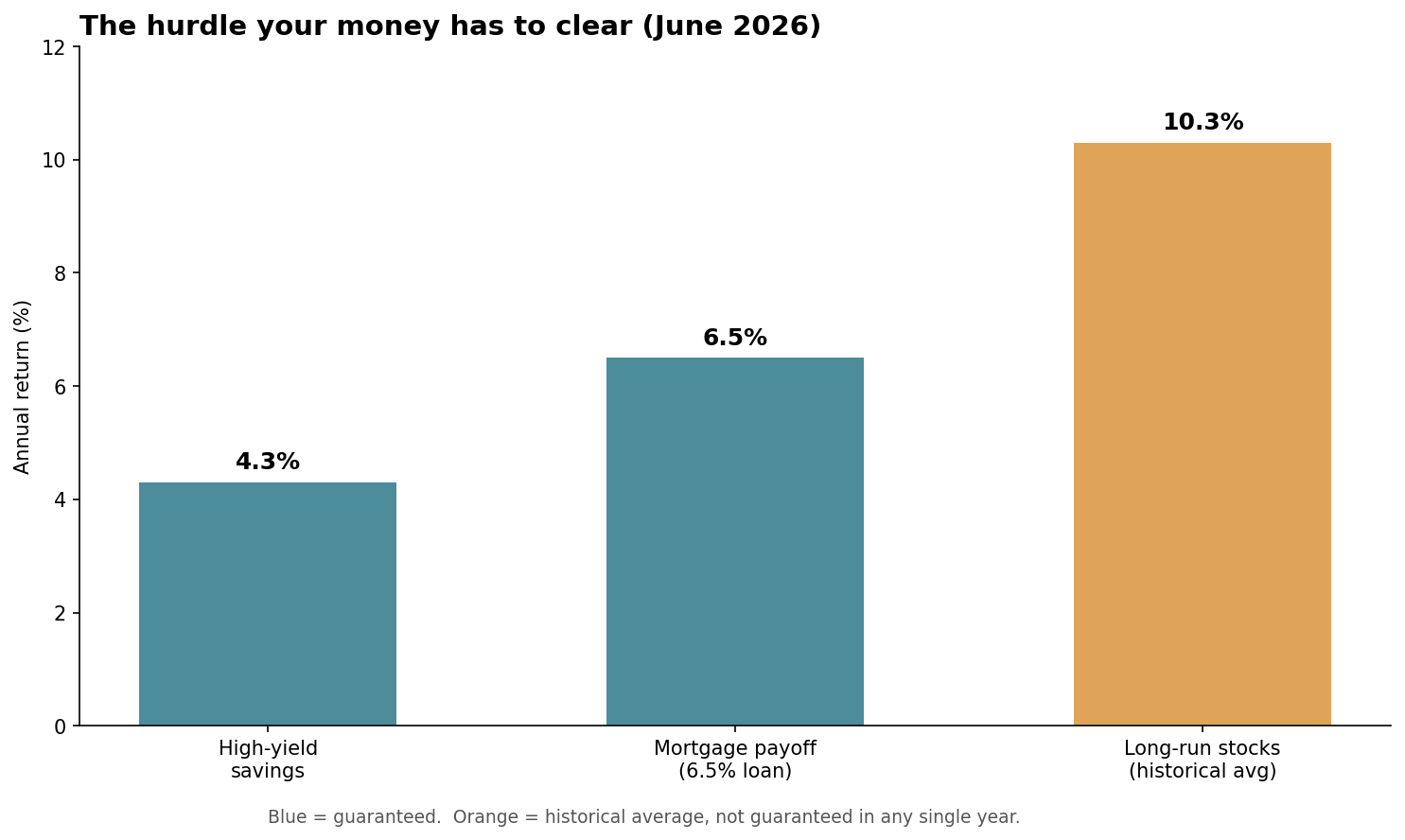

Paying off your mortgage is one of the few guaranteed returns in personal finance. Every extra dollar of principal you pay erases future interest at exactly your mortgage rate. If your loan is at 6.5%, an extra payment "earns" you 6.5%, risk-free, with no market to worry about. That rate is your hurdle rate, the number any investment has to clear to be worth choosing instead.

Investing can clear it, but not with certainty. According to Fidelity's overview of long-run stock market returns, the S&P 500 has averaged about 10% a year since its inception, with dividends reinvested. That is comfortably above a 6.5% hurdle. The catch is the word "average." Almost no individual year actually lands near 10%, and the opportunity cost of paying down a low-rate loan only stings if the market cooperates over your specific time horizon.

Figure 1: Bar chart comparing annual returns from high-yield savings at 4.3%, mortgage payoff at 6.5%, and the long-run stock market average at 10.3%.

So the maths reduces to a clean rule of thumb. If your mortgage rate is meaningfully below your expected return, lean toward investing. If your rate is close to or above the return you can reasonably expect, paying down the mortgage looks better and comes with zero risk. The closer the two numbers sit, the more the tiebreakers below decide it.

Why today's mortgage rate can flip the answer

Rates are the reason this question is live again. Freddie Mac's weekly mortgage rate survey put the average 30-year fixed mortgage at 6.47% in mid-June 2026, with the 15-year fixed at 5.81%. That is a world away from the sub-3% loans of 2021.

Think about what that does to the comparison. At a 3% mortgage, your hurdle rate is tiny and almost any diversified portfolio is expected to beat it over time, so investing wins easily. At 6.5%, the hurdle is high enough that paying down the loan is genuinely competitive with stocks and far ahead of cash or bonds. The exact same person, with the exact same risk tolerance, should reasonably make a different choice depending only on the rate stamped on their loan.

This is why blanket advice fails. "Never pay off a mortgage early" was close to right in 2021. It is shaky in 2026. Pull up your own rate before you do anything else, because that single number moves the answer more than any opinion online.

The tax angle most guides get wrong

Older articles lean hard on the mortgage interest deduction, telling you that paying off your loan early throws away a valuable tax deduction. For most people in 2026, that argument is simply out of date.

To deduct mortgage interest at all, you have to itemize, and you only itemize when your deductions beat the standard deduction. The 2026 standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly, per the IRS figures. Those amounts are so high that roughly 9 in 10 filers now take the standard deduction and never itemise at all. If you take the standard deduction, your mortgage interest gives you no tax benefit, so the "lost deduction" costs you nothing.

The deduction still helps a minority. If you have a large loan, a high rate, and enough other write-offs to clear the standard deduction, the rules in the IRS guide to the home mortgage interest deduction let you deduct interest on up to $750,000 of mortgage debt. For that group, the after-tax cost of the mortgage is lower than the headline rate, which nudges the maths back toward investing. Most readers are not in that group, so check your own return rather than assuming.

One more tax point cuts the other way. Money you invest in a taxable brokerage account can owe capital gains tax when you sell. Long-term gains are taxed at 0%, 15%, or 20% depending on income, and the 2026 capital gains brackets start the 15% rate above $49,450 for single filers and $98,900 for couples. Paying off your mortgage, by contrast, produces a return no one taxes. A guaranteed 6.5% with no tax is worth more than a 6.5% taxable return, which quietly tilts the field toward payoff for money that would otherwise sit in a taxable account.

The behavioural overlay: the sleep-at-night return

The maths gets you most of the way. The rest is about you, and pretending otherwise leads people to plans they abandon at the worst moment.

A paid-off house is not just a financial position. It lowers your fixed costs to almost nothing, which changes how a job loss or a recession feels. Being debt-free has a real return that never shows up in a spreadsheet: you sleep better, you take less career risk to cover a payment, and you are far less likely to panic-sell investments in a downturn just to make ends meet. If a 1% lower expected return buys you the calm to stay invested, that trade can be worth it.

Your risk tolerance matters here, and so does sequence of returns risk, which is the danger of hitting a bad stretch of market returns early, right when you are counting on the money. Two people can run identical numbers and land in different places. Someone who watched a parent lose a home, or who knows they will bail out of stocks the first time the market drops 30%, gets a higher real return from the certainty of payoff than the spreadsheet suggests. Someone calm, young, and decades from needing the money can lean further into investing without losing sleep. Be honest about which one you are.

Extra mortgage payments or invest: a worked example

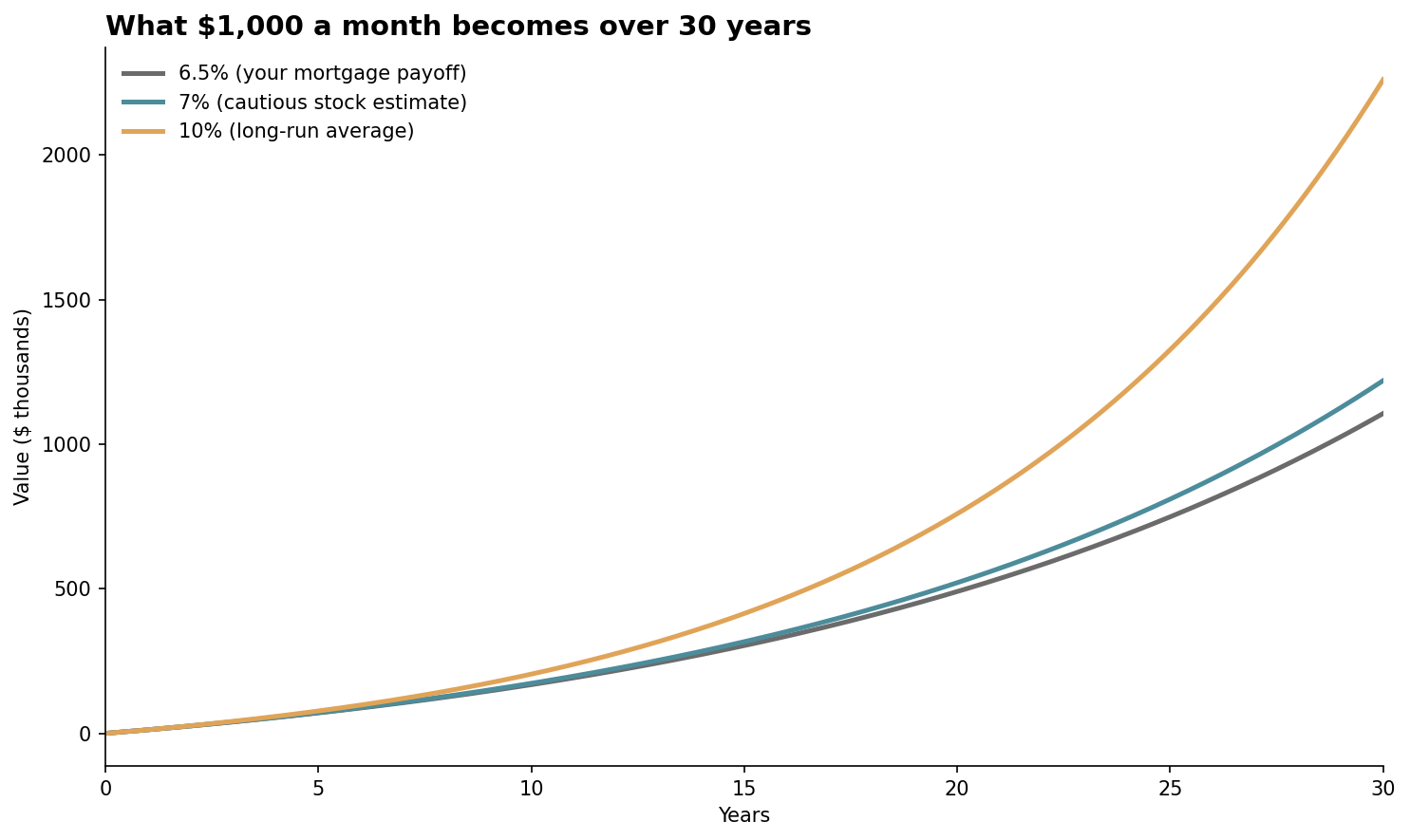

This is easier with a real person. Meet Maya, 30, who just bought her first home with a 6.5% mortgage and has $1,000 a month of genuine extra cash after covering the match, her high-interest debt, and a full emergency fund. Should she throw it at the loan or the market?

If Maya could lock in each of three returns on that $1,000 a month for 30 years, here is roughly where she lands:

Figure 2: Line chart showing the growth of $1,000 invested monthly over 30 years at 6.5%, 7%, and 10% annual returns.

- At 6.5%, the guaranteed equivalent of paying down her mortgage, she ends near $1.1 million of value, with zero risk along the way.

- At 7%, a deliberately cautious stock estimate, she ends near $1.2 million. Close to payoff, but not certain.

- At the long-run 10% average, she ends near $2.3 million. A huge gap, but only if the market actually delivers that average over her specific 30 years.

The spread between the guaranteed line and the 10% line is the prize for investing. The distance between the guaranteed line and the 7% line is how thin that prize gets once you use a sober return estimate. Maya's real choice is whether the chance at the top line is worth giving up the certainty of the bottom one. For her, young and steady, leaning toward investing is reasonable. For someone five years from retirement, the same chart argues for more payoff, because there is less time to recover from a bad sequence.

If you want to run your own version, the Alpha Investing Group index investing calculator and the mortgage payoff calculator let you plug in your real rate and time horizon instead of Maya's.

The hybrid most people should default to

You do not have to pick a side. The most durable answer for most homeowners is to split the extra money, and it is the option almost every "pick one" guide skips.

Send part of your spare cash flow to the mortgage and part to a low-cost index fund. You bank the guaranteed return and the calm of a shrinking loan, and you keep real exposure to the market's upside. A 50/50 split is a sensible default. If your rate is high, say above 7%, tilt more toward payoff. If your rate is low and you are young, tilt more toward investing. If you are brand new to the market side, our guide to index investing for beginners walks through how to set that part up without picking stocks.

The hybrid also protects you from being wrong. Nobody knows the next decade's returns. Splitting means you are never fully exposed to the one outcome that would have made the other choice obviously better in hindsight.

In summary

The decision to pay off mortgage or invest is a calculation with a human tiebreaker. Run it in this order:

- Clear the prerequisites first. Capture the full 401(k) match, kill high-interest debt, and fund three to six months of expenses before you choose.

- Compare two numbers. Your mortgage rate is your guaranteed return and your hurdle rate. Your expected investment return is what you give up by paying down the loan. The bigger number usually wins.

- Check today's rate. At 6.5% the hurdle is high, so payoff is competitive in a way it was not at 3%.

- Don't over-weight the tax break. Most filers take the standard deduction and get no mortgage interest deduction at all.

- Be honest about yourself. The sleep-at-night value of being debt-free is real, and your risk tolerance changes the right answer.

- When in doubt, split. A 50/50 default banks the guaranteed return and keeps your upside.

Pull up your mortgage rate, decide whether you are a payoff person or a market person, and if you cannot decide, do both. That is not a cop-out. It is usually the smartest move.

Frequently asked questions

At what mortgage rate should I pay it off instead of investing?

There is no universal cutoff, but the rate changes the lean. Below about 4% to 4.5%, the hurdle is low enough that most people are better off investing. Above about 6% to 7%, paying down the loan is a strong, guaranteed return that is hard to beat safely. In the wide middle, the tiebreakers, your taxes, your risk tolerance, and your peace of mind, decide it.

Should I pay off my mortgage before maxing my 401(k)?

Capture your full employer match first, every time, because that is an instant return no mortgage payoff can match. Beyond the match, it becomes a closer call. Tax-advantaged retirement space is valuable and you lose it if you do not use it that year, so many people fund retirement accounts before making extra mortgage payments. Paying down the loan ahead of unmatched retirement contributions is mainly for people who place a high value on being debt-free.

Does paying off my mortgage hurt my access to cash?

Yes, and it is the most underrated risk. Money you put into your home is hard to get back out. You would need to sell or borrow against the house, which takes time and may not be possible exactly when you need it. Money in a brokerage account, by contrast, can be sold in days. This is why an emergency fund comes before extra mortgage payments, and why locking up every spare dollar in the house can leave you cash-poor.

What if rates fall and I could refinance?

If rates drop enough to refinance, your decision can change with your new rate. A lower rate means a lower hurdle, which tilts the maths back toward investing. It usually makes sense to wait and see where your rate settles after a refinance before committing to an aggressive payoff plan, since you do not want to overpay a loan you are about to replace with a cheaper one.