Should Your Index Fund Include the Whole World, or Just America? Here's the Honest Trade-off

This page may contain some affiliate links. This means that, at no additional cost to you, Alpha Investing Group will earn a commission if you click through and make a purchase. Learn more.

Whole world or just the US? The short version

You've opened a brokerage account, picked a fund, and then hit the one question nobody warned you about. Should your index fund hold only U.S. companies, or the whole planet?

It feels like a high-stakes call. The choice between a U.S. index fund and an international index fund gets framed online as a fork in the road, with one path leading to riches and the other to regret. Most of the heat comes from people pointing at whichever side has done better lately. And almost none of it gives you something you can actually act on and then forget about.

Here's the honest version. This is a smaller decision than the internet makes it look, and you can settle it in an afternoon.

By the end of this guide you'll have:

- A clear read on the real case for US-only and the real case for global

- The catch that most beginner guides skip entirely

- A simple, research-backed rule for how much international to hold

- A way to lock the decision in so you stop second-guessing it

What a US vs international index fund decision actually comes down to

Strip away the noise and you're really choosing between two boxes.

One box holds American companies. The other holds everything else: Japanese carmakers, European banks, Taiwanese chipmakers, Brazilian miners. A US total-market fund buys the first box. A total world fund buys both, weighted by size. An international fund buys only the second box, which you'd hold alongside a US fund.

That's the whole machine. Everything else is a debate about how much of each box to own.

The case for keeping it US-only

The US-only argument is stronger than global investors like to admit.

Start with size. The American market is the deepest and most liquid on earth, and it's home to most of the world's largest companies. By the official tally in SIFMA's 2025 Capital Markets Fact Book, U.S. equity markets make up close to half of all global stock market value. When you buy the S&P 500, you already own businesses that earn a large slice of their revenue overseas. Apple sells phones in Shanghai. Coca-Cola sells drinks in Lagos. You're getting global demand without leaving home.

Then there's cost and simplicity. A US total-market fund is about as cheap as investing gets, and you only have one thing to track. Fewer funds means fewer decisions, and fewer decisions means fewer chances to do something dumb. For a beginner building their first portfolio of low-cost index funds, that simplicity has real value.

The honest weakness: this is a bet, even if it doesn't feel like one. Betting everything on your home country has a name, home bias, and it's still a concentrated position. It just happens to be the position that's paid off for the last fifteen years.

The case for owning the whole world

The global argument rests on one uncomfortable idea. You don't know which country wins next.

Diversification is the only free lunch in investing, and going global is diversification at the largest possible scale. Markets outside the US don't move in perfect lockstep with it, so owning both can smooth out the ride. Vanguard's guidance on international investing makes the point bluntly: skipping international isn't the safe choice, it's a concentrated one. The same page splits the non-US world into developed markets like the UK, Japan, and France, and faster-growing, choppier emerging markets like India and Brazil, which it pegs at roughly 15% to 25% of the international total.

There's also the recency trap. US stocks have crushed international for over a decade, which makes US-only feel obviously correct. But "what worked recently" is exactly the wrong reason to pick an investment. The 2000s, often called the lost decade for US stocks, ran the other way: American shares went roughly nowhere while international and emerging markets did well. Whoever skipped international going into that decade learned the lesson the expensive way.

Owning the whole world is really just an admission of humility. You're saying you can't predict the next winner, so you'll hold all of them. That instinct sits at the center of building a diversified portfolio that you don't have to babysit.

The catch nobody mentions: a total world fund is still mostly America

This next part quietly reframes the whole argument.

A total world fund is built on market cap weighting, which means each country shows up in proportion to its total stock value. Because the US is so large, that single fund lands at roughly 60% US and 40% everything else. So when someone says "just buy the world and stop worrying," what they're actually recommending is a portfolio that's still mostly American.

Sit with that for a second. A "total world fund" and an S&P 500 fund are not opposites. They overlap heavily. The world fund moves largely in step with the US market for the simple reason that the US is most of it. The genuine difference is that 40% slice of non-US companies, and whether having it changes your outcome enough to matter.

This is why the US-vs-global fight is quieter than it sounds. The two reasonable choices aren't "all America" versus "no America." They're "all America" versus "mostly America." That's a far smaller gap than the arguments suggest.

What the data says, and why you can't time it

People reach for performance charts to win this argument. The charts don't settle it. They prove the opposite.

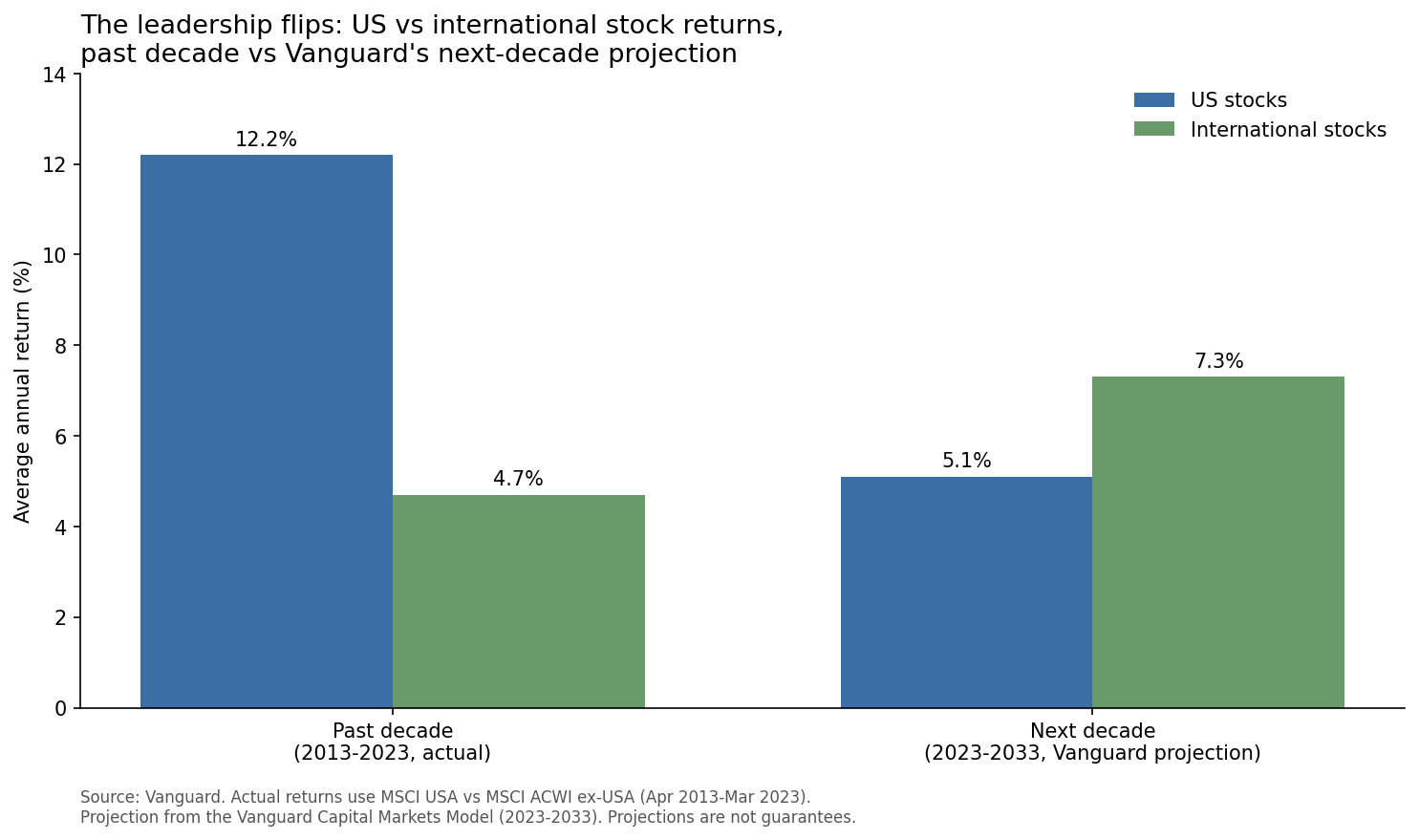

Look at the last completed stretch. Vanguard's analysis of international equity allocations found that from April 2013 to March 2023, US stocks returned about 12.2% a year while international returned about 4.7%. That's a 7.5 percentage point annual gap, and it's the run that made US-only look like a no-brainer. A strong dollar and rising US valuations drove most of it.

Now look at what the same firm projects next. Vanguard's model has the relationship flipping, with US stocks at roughly 5.1% a year and international at 7.3% over the following decade. Their own words: international outperformance "is far from guaranteed." That hedge is the honest part.

Grouped bar chart comparing average annual returns of US and international stocks.

The takeaway isn't "international is about to win." It's that two snapshots ten years apart point in opposite directions, and a respected research team won't bet the house on its own forecast. If the professionals treat this as barely better than a coin flip, you should treat your own confident hunch with suspicion.

One more wrinkle to hold honestly: currency risk. When you own international stocks as a US investor, a strengthening dollar quietly drags on your returns and a weakening dollar quietly lifts them. It cuts both ways over time, but it adds noise that a US-only investor never sees.

How much international should you actually hold?

So you're not choosing all-or-nothing. You're choosing a dial setting. Here's where to set it.

The research lands on a range, not a magic number. Vanguard's guidance on international investing recommends holding at least 20% of your stock money in international, and about 40% to capture the full diversification benefit. Most of the smoothing benefit shows up by the time you reach 20%, with diminishing returns as you push past 50%. A pure market cap weighting, the "own the world as it actually is" approach, puts you near 40%.

That gives you three defensible settings:

- The market-weight setting (about 40% international). You hold the world in its real proportions and make no active call. A single total world fund does this for you automatically.

- The middle setting (around 30%). Enough international to matter, tilted a little toward the home market most US investors are comfortable with. A common, sensible compromise.

- The light setting (about 20%). The research-backed floor. You still get most of the diversification benefit while keeping the portfolio US-heavy.

Anything below 20% starts giving up the benefit the research actually supports. Anything in the 20% to 40% band is reasonable, and the difference between those endpoints is not worth losing sleep over. If you want broader emerging-markets exposure inside that international slice, that's a separate dial you can read up on in our guide to emerging-markets investing.

Notice what's not on this list: 0%, and 100% international. Both are bets that you know something the market doesn't.

Pick once, then stop second-guessing

The worst version of this decision is the one you keep making.

Every January, some article will tell you international is finally back, or that the US is unstoppable, and you'll feel the urge to flip your allocation. Don't. The cost of bouncing between strategies is almost always higher than the cost of picking a merely-fine one and holding it. This is the core idea behind passive index investing: the discipline beats the tinkering.

So make the call, write it down, and walk away. Pick a number between 20% and 40%, or just buy a single total world fund and let market cap weighting decide for you. Then automate your contributions and check in once a year, not once a news cycle.

The investors who do best with this question aren't the ones who guessed the next decade right. They're the ones who picked a reasonable split and then got bored with it.

In summary

If you want the whole guide as a checklist:

- The real choice is "all America" vs "mostly America." A total world fund is still about 60% US, so the gap between the options is smaller than the debate implies.

- Performance charts can't settle it. US led by 7.5 points a year to 2023. Vanguard projects that reversing, and won't guarantee its own forecast.

- Hold 20% to 40% of your stock money internationally. That's the research-backed band. Most of the benefit lands by 20%, and market weight sits near 40%.

- Mind the small stuff. International adds currency risk and a slightly higher expense ratio, neither of which is a dealbreaker.

- Decide once and automate. The discipline of holding your split beats the instinct to chase whichever side just had a good year.

The honest answer to "whole world or just America" is that both can work, the difference is modest, and the biggest risk isn't picking the wrong split. It's never committing to one.

Frequently asked questions

Do I even need an international index fund if I already own an S&P 500 fund?

You don't strictly need one, and you'll be fine without it. But an S&P 500 fund is a bet on a single country, even though it owns global-facing companies. Adding international gives you genuine diversification across economies that don't all rise and fall together. The research says somewhere between 20% and 40% of your stock allocation is a reasonable place to land.

How much of my portfolio should be international?

Vanguard recommends at least 20% of your stock money in international, and about 40% to get the full diversification benefit. A pure market cap weighting, which is what a total world fund gives you automatically, puts you near 40%. Anywhere in that 20% to 40% band is defensible, so pick a number and stick with it.

International stocks have lagged for years. Why hold them at all?

Because "lagged recently" is the worst possible reason to drop an investment. US stocks beat international by about 7.5 percentage points a year over the decade to 2023, but the 2000s ran the opposite way during the lost decade for US shares. Vanguard's own model projects international outperforming over the next decade, while admitting that's far from guaranteed. Holding both is an honest admission that you can't time the switch.

Are international index funds more expensive than US ones?

Usually a little, yes. International funds tend to carry a slightly higher expense ratio than the cheapest US funds, because trading across foreign markets costs more. The difference is typically small, often a fraction of a percent, and not a reason to skip international on its own. A broad total world fund keeps costs low while doing the diversification for you. You can compare options in our roundup of low-cost passive funds.

This article is educational and not personalized investment advice. Index funds carry risk, including possible loss of principal, and past performance doesn't predict future results.