Investing

What is Financial Literacy?

This page may contain some affiliate links. This means that, at no additional cost to you, Alpha Investing Group will earn a commission if you click through and make a purchase. Learn more.

Money is by no means the most important element of our lives. However, it is undeniably a crucial piece of the puzzle. It is incredibly difficult to live a fulfilling life if you are troubled by money problems every day.

T. Harv Eker, the author of the Secret of the Millionaire Mind, once said, "The single biggest difference between financial success and financial failure is how well you manage your money." To master money, you must first manage money. Hence, become financially literate is the best way to solve all your money problems.

In this article, I will explain:

- What is financial literacy?

- Why is financial literacy important?

- Why should you improve your financial literacy now more than ever?

Last but not least, we have prepared a financial literacy test to help you assess your financial literacy. Excited already? Start reading now!

What is financial literacy? The financial literacy definition

Simply put, financial literacy is the knowledge of money. It is anything you need to know about money. It ranges from something basic such as understanding how a saving account works, to technical topics like how to diversify your investment portfolio.

Financial literacy is the ability to understand different financial products and make informed financial decisions. We make financial decisions every day. Making financial decisions is an integral part of our lives. The main difference between a financially literate person and one who is not is that the former is able to make the right financial decisions.

Having said that, there is no one correct answer for financial problems. A person can put their money in a savings account, and another can invest it in the stock market. As long as they understand the financial products, their financial goals, and risk tolerance and make their decisions based on those factors, they are both making financially literate decisions.

Money can be a stressful topic to talk about, but it does not have to be that way. Especially after you understand it. Once you comprehend the idea, feel free to discuss this topic with the people around you. Get their views and opinions, understand what they think and where they are coming from, and before you know it, “money” will be the most exciting topic to talk about. Financial literacy is the key to achieve financial success. Hence, the earlier you start, the better. But hey, you are already reading this!

Why is financial literacy important?

Now you have understood the financial literacy definition, let's take some time to talk about why it is important. There are 4 points that I would like to emphasize:

-

Financial literacy helps you to choose the right financial products.

Most financial products seem complicated nowadays as we do not understand how they work. Ask yourself, how do you choose the right products if you don't even understand what you are dealing with?

Take the most simple financial product — the credit card as an example. Credit cards allow you to borrow money from the bank, up to a certain limit, and pay it back at a later time. There are two ways that you can pay the money back:

- You can pay it back in full every month, in which case you would not need to pay any interest;

- Or you can make a payment that is at least the minimum payment every month.

If you keep paying the minimum due every month, it would take you six years and seven months to pay off the debt! Furthermore, you would have paid $2,009.55 for your $1,000 debt! That means you are paying $1,009.55 in interest. That's even MORE than your debt!!! Compared to paying the $1,000 in full in the first month, it is needless to say which is the better financial decision. The question is, however, are you able to make the right one?

On the face of it, it might not look all different. In fact, the second option might seem better since you get to pay back your debt in small chunks. The reality, however, is an entirely different story.

Let's say you have successfully applied for a credit card with a credit limit of $2,000 and an annual percentage rate (APR) of 25%. You spent $1,000 on a laptop and got your credit card bill at the end of the month. Instead of paying off $1,000 in full, you decide that paying the $30 minimum due is a better choice.

This example fully indicates that poor financial decisions can cost you a FORTUNE! Believe it or not, without being financially literate, you will be making poor financial decisions in your everyday life.

-

Financial literacy is the key to secure your retirement.

Let's face it, getting a financially supported retirement is not an easy task. For the past ten years, wage growth has hardly kept up with inflation. Most people can't get their retirements even after working for more than 40 years, 9 to 5 (or more!) five days per week.

And the key? Financial literacy. Look, retirement is not about how much you earned. It's about how you manage and invest the money you have earned. I am not saying that not don't have to work and earn. But if getting a retirement is what you want, managing and investing your money wisely plays a more critical role.

To manage money wisely, you need to be financially literate. To invest rationally, you need to be financially literate. There is no other way.

-

Financial literacy will also secure the financial future of your next generations.

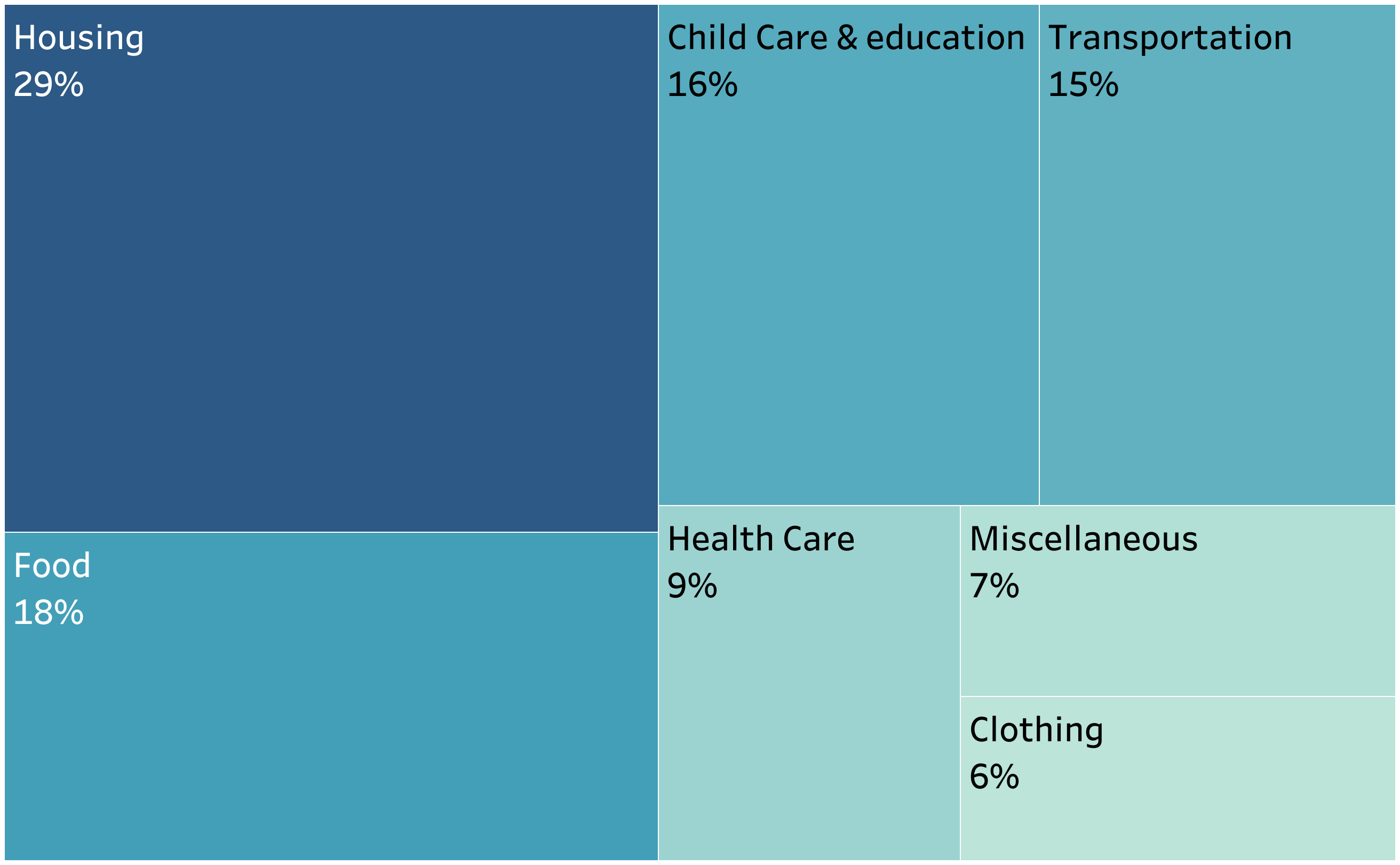

According to research, a family spends $233,610 to raise a child from age 0 to 21 in the US and £253,638 in London. The following chart gives you a detailed breakdown of how the money is expected to be spent.

Figure 1: Cost breakdown to raise a child, source: U.S. Department of Labor and U.S. Department of Agriculture

It should be clear now that raising a child requires detail and shrewd financial planning. If you can't even plan your financial future, how are you going to plan for your sons' or daughters'? -

Financial literacy is your best weapon against financial recession.

Financial literacy might not seem crucial when the markets are trending upwards and you are making lots of money. However, when a recession happens, what are you going to do? If the value of your investments plummet by 20% overnight, will you panic? Should you hold or sell? Or buy more?

Without financial literacy, it is impossible to answer those questions. Hence, it is not surprising to see most people panic-sell when the market is going down. When you don't understand a thing about investment, your best choice would be to do what everyone seems to be doing, which is the worst choice you can make most of the time.

Making the right financial decisions is important, and even more so during recessions. Hence, to survive recessions, you have to be financially literate.

Why should you improve your financial literacy now more than ever?

So, financial literacy is important, but when should you start looking into it? I would encourage you to start improving your financial literacy right now. Why? The reasons are simple:

- Saving can no longer bring you wealth.

- Spending is getting easier.

- Investing is getting more complex.

Let me paint you the picture by stating some facts.

-

Spending has never been easier. And it all comes down to two main factors — temptations and low “entry barrier”.

The booming social media has made the marketing of products ever so efficient. Facebook spends ~$8.5 billion per year to pay for engineers to design software that will allow sellers to understand what you like and what you need most. It is now easier than ever for them to target all their marketing effort just to convert you to their customers. In fact, a lot of people feel like they want to buy everything they see online.

And guess what? It doesn't take long for the banks to formulate their strategies to capitalize on this opportunity.

How do they do it? Simple. All they need is to allow people to spend their money easier. In other words, lower the threshold or barriers to buying.

The easiest way to achieve this is to make it easier for people to apply and get a credit card. From the example above, we already know how detrimental credit cards can be to our lives if we are not financially literate from the example above. You can easily get into debt.

To make it worse, the banks allow you to apply for a new credit card by transferring your existing credit card debt with a lower interest rate once you have spent all your credit limit.

A lot of people see this as their last straw. However, after their transfer their debt, they continue to overspend as soon as they know they have more credit limit. This situation can easily snowball anyone into a huge credit card debt that one can never repay.

-

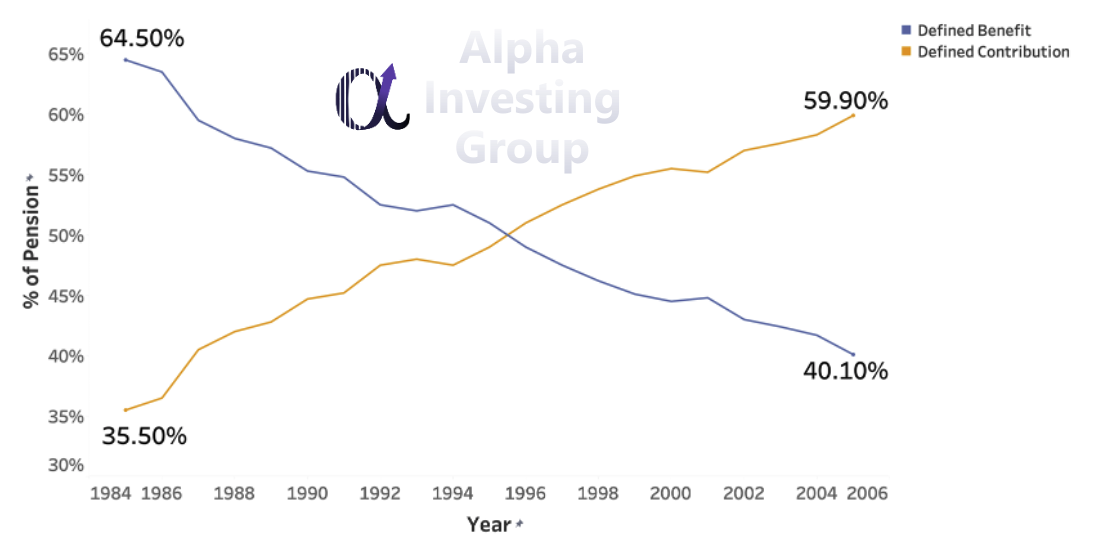

Starting in the late 90s, pension schemes around the world have been going through some significant changes. What used to be defined benefit pension schemes are now shifting rapidly to defined contribution pension schemes.

With a defined benefit pension plan, you are guaranteed to get a certain amount of money every month when you retire. The company you worked for will bear the investment risks.

However, with a defined contribution pension scheme, you will be the one bearing the investment risks. You and your employer will both contribute to the plan, but no one is sure how much money you will end up getting when you retire. It totally depends on the performance of the pension fund.

This essentially means your retirement is now officially unpredictable. If you did not choose a pension fund that matches your risk tolerance and return requirements, you might end up having very little money in your pension when you retire.

As shown in the graph below, 65% of the pension asset used to be defined benefit in 1985. The number quickly decreased to 40% in 2005, and the trend is continuing and accelerating.

Figure 2: The evolution of defined benefit and defined contribution pension funds, source: U.S. Federal Reserve Board

So, to have a financially supported retirement, you will have to be financially literate because many crucial decisions, such as the contribution you should make, what pension fund to choose, need to be made.

-

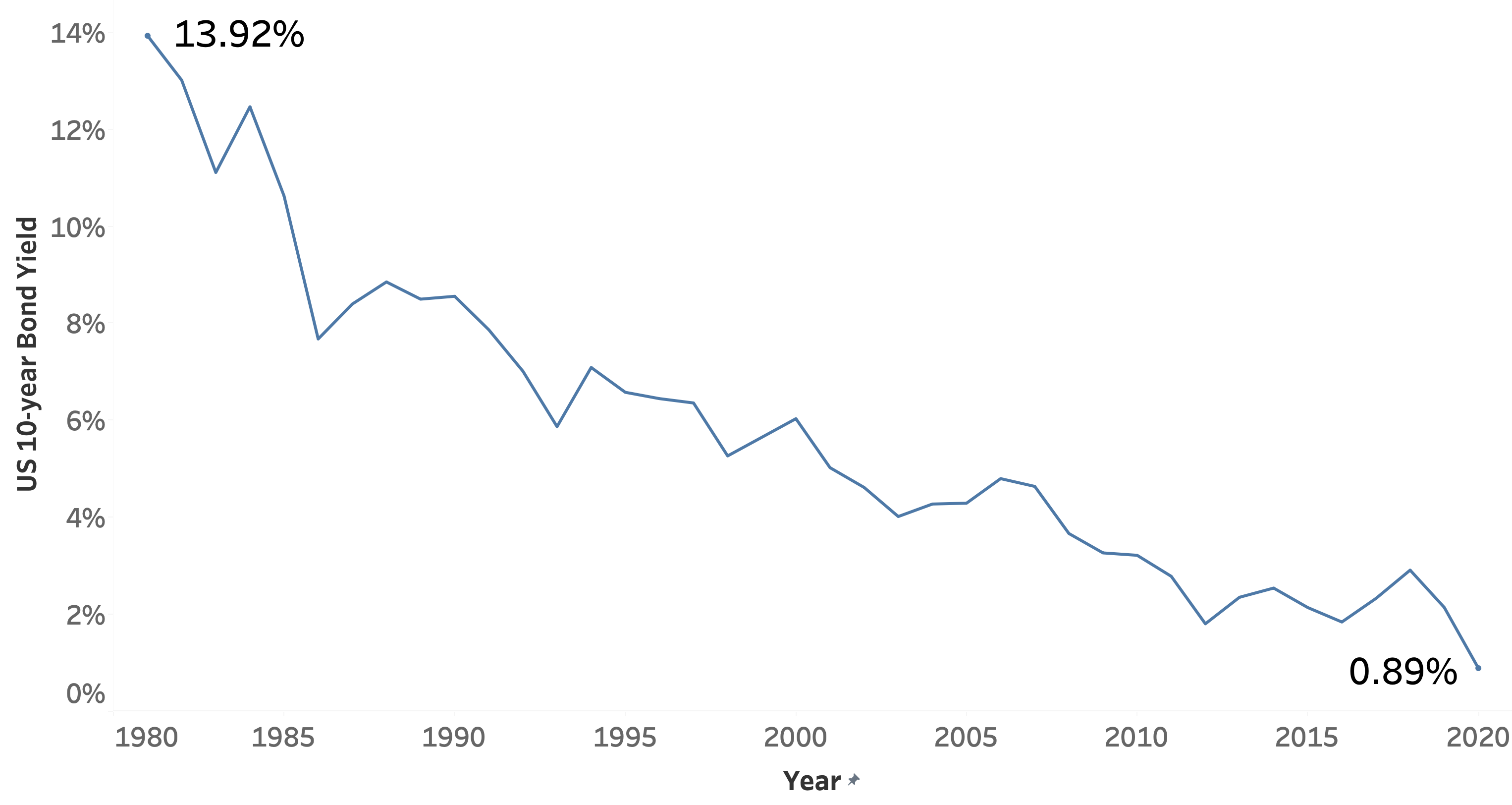

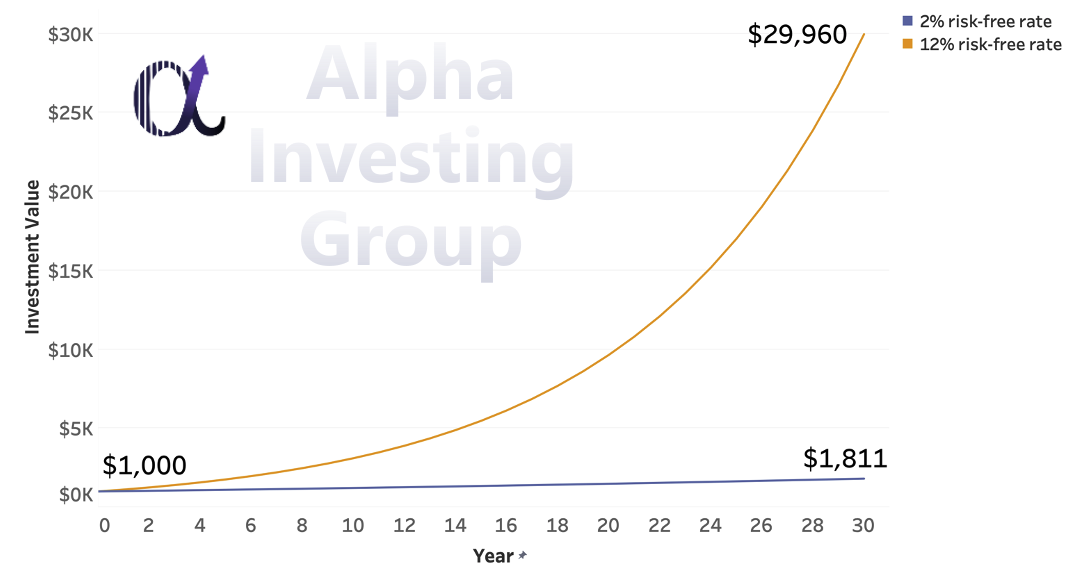

You would think I am crazy if I have told you that it is getting harder to earn a return by investing nowadays compared to 30 years ago. But it is true. Just look at the graph below. The US 10-year bond yield used to be around 12% in the 80s, and it has been barely 2% in recent years.

Figure 3: The U.S. 10-year bond yield since year 1990, source: US Department of the Treasury

What's the difference? It means if you invest in the US 10-year bonds for 30 years, you will get 16.5 times less! And if you think about it, you can no longer rely on risk-free investments such as the US 10-year bond for your retirement since the bond yield is lower than the inflation most of the time. It means that you are actually losing money by investing in the US 10-year bonds.

Hence, to achieve decent returns, you have no other choice but to choose a riskier (it may not have to be risky, but it is no longer risk-free) path, such as investing in the stock market. Needless to say that, if you are not financially literate, you would be gambling instead of investing in the stock market.

Figure 4: Investment results with 2% and 12% risk-free rates, source: Alpha Investing Group Research

Figure 4: Investment results with 2% and 12% risk-free rates, source: Alpha Investing Group Research -

The threshold to access financial products is at its all-time low. With the FinTech industry booming, retail investors like us are given increasingly more opportunities to invest in different financial products. With some of the online brokers, you can start investing with as low as $1.

Furthermore, financial products that are accessible to the public are getting more complex. It is no longer just investing in stocks and major indices. Nowadays, almost everyone can invest in ETFs. In some of the countries, retail investors can even invest in complex financial instruments such as options.

These financial products can allow you to generate great investment returns. However, to generate consistent returns, you need to understand them. Otherwise, you are relying on sheer luck. Needless to say, that is an awful decision, especially when you are investing your savings.

Are you ready to be financially literate?

Hopefully, by now, the picture I am trying to portray is a lot clearer — financial literacy is the key to financial freedom and ultimately to a more fulfilled life. No one has ever depicted the importance of financial literacy better than the legendary Alan Greenspan, "The number one problem in today's generation and the economy is the lack of financial literacy."

Now, aren't you curious about how financially literate you are? It is time for you to assess your financial literacy by taking our financial literacy test. This financial literacy quiz can tell you how financially literate you are.

What's next? To improve your financial literacy, explore the Alpha Investing Group. With the financial knowledge we provide, we aim to bring you the best financial education. It is your best financial literacy course. You can also check out the best personal finance books that we have picked for you.

We believe a financially literate world is a better place. It is a place where people can achieve their dreams and secure their future.

It's the world we want to help build.